Thinking About Leasing Your First Car? Here’s How to Not Get Lost in the Fine Print

If you’ve never leased a car before, the whole thing can feel like a different language. Big numbers, weird terms, a payment that sounds amazing until you read the small print under it. Don’t worry. Leasing is actually pretty simple once someone walks you through it, and that’s what this is.

Leasing a Car: Quick Tips

New to leasing? Here are the basics of what you need to know.

-

Look past the monthly payment. Add the cash due at signing, divide by the months, and compare that real number instead.

-

Skip the big down payment. It barely lowers your payment and builds no ownership, so keep your cash in your pocket.

-

Pick the right mileage upfront. Going over costs extra at turn-in, so tell us how you actually drive and we’ll set you up right.

Below, we’ll dig into each of these in more detail.

So what is a car lease, exactly?

A lease is a long-term rental for a car. You make a monthly payment, drive it for two or three years, then hand it back and either lease something new or walk away. Think rental, not purchase.

The upside: your monthly payment is usually lower than buying the same car. The trade-off: you don’t own anything at the end.

And here’s something that makes this whole process way less stressful: Walser is a no-negotiation dealer. That means the price is the price. It’s the same for everyone, there’s no haggling, and nobody’s going to pressure you or play games to see how much you’ll pay. So you can skip the part where you’re supposed to “talk them down” and just focus on understanding whether a deal actually fits you. That’s the part that matters anyway.

New to leasing? This guide breaks down how it works, how it stacks up against buying, and exactly what to check before you sign.

Jump to any term you want to understand:

- Effective Monthly Cost

- Due at Signing

- Residual Value

- Money Factor

- Mileage Allowance

- Term Length

- Cap Cost

- Cap Cost Reduction

- Acquisition Fee

- Disposition Fee

- Drive-off Fees

- Loyalty or Conquest Cash

See This Month’s Lease Offers

Now that you know what makes a good lease, take a look at what’s available right now. The price you see is the price, no haggling, no pressure. Find the one that fits how you actually drive.

What Do I Need to Know Before Leasing a Car?

The big mistake first-time leasers make is shopping by the monthly payment alone. A car ad will scream “$199 a month!” in huge letters, and that sounds great, until you notice the tiny text that says you have to hand over $5,000 the day you sign.

Here’s the thing: a $199 payment with $5,000 due upfront actually costs you more than a $279 payment with nothing down. The low monthly number is bait. So the first skill to learn is looking past it.

The Numbers That Actually Matter

You don’t need to be a math person. You just need to know what these few things mean.

Effective monthly cost: This is the one that cuts through all the marketing. You take everything you’ll pay over the whole lease, including any cash you put down at the start, and divide it by the number of months. That tells you what the car truly costs you each month. For example, a car advertised at $209 a month, but with $4,299 due upfront on a three-year lease, really costs you closer to $328 a month once you spread that big upfront chunk across the term. Always figure this out before comparing two deals, because it’s the only fair way to line them up.

Due at signing: This is your upfront money, which covers your first payment, some fees, taxes, and any down payment you choose to make. Lower is almost always better. And here’s a tip a lot of people don’t know: putting a big down payment on a lease feels smart, but it usually isn’t. Since you don’t own the car, that money isn’t building toward anything. And if the car gets totaled or stolen early in the lease, that down payment is just gone. You don’t get it back.

Residual value: This is what the car is expected to be worth at the end of the lease. It sounds technical, but it’s actually the secret behind why some cars are way cheaper to lease than others. A car that holds its value well (like a Toyota Tacoma) is cheaper to lease, because you’re only paying for the value it loses while you have it. Cars that lose value fast cost more to lease. So sometimes a more expensive car has a cheaper lease payment, and now you know why.

Can I buy the car at the end of the lease?

Yes, and this is where residual value comes back around. Most leases give you the option to buy the car when the term ends, and the price is usually that residual value set at the start. So you have a few choices when the lease is up: hand the car back and walk away, lease something new, or buy the one you’ve been driving for its residual price. Buying out makes the most sense if you’ve grown attached to the car, you’ve put extra miles on it (since buying it cancels out any overage fees), or the car is actually worth more than the residual on the open market. In that last case you’d be buying it for less than it’s worth, which is a nice spot to be in. No rush to decide now, just know the option is there.

Money factor: A lease has an interest cost just like a loan does, but instead of showing it as a percentage, it’s written as a tiny decimal like 0.00125. If you ever want to translate it into a normal-sounding interest rate, multiply it by 2,400. So 0.00125 works out to about 3 percent. You don’t have to memorize this, just know it exists so it doesn’t catch you off guard.

Mileage allowance: Every lease comes with a yearly mileage limit, usually 10,000 or 12,000 miles. If you go over, you pay a fee for every extra mile, often 15 to 25 cents each, when you turn the car in. That adds up fast. So if you’ve got a long commute or you road-trip a lot, ask for a higher mileage limit from the start. Paying a little more upfront is way cheaper than getting hit with a big bill at the end.

Term length: Most leases run 24 to 36 months (two to three years). If you see a weird length like 18 or 39 months, just be a little curious about it. A super-short lease can show a low monthly payment but pack your fees into a shorter window. A longer one can lower the payment in a way that isn’t always the bargain it looks like. Neither is automatically bad, just worth a second look.

A Few Terms You’ll See on the Paperwork

These words sound intimidating but they’re simple once translated:

- Cap cost: the price of the car your lease is built on. At a no-negotiation dealer like Walser, this is set up front and is the same for everyone, so you don’t have to worry about whether you got a worse deal than the next person.

- Cap cost reduction: a fancy way of saying any down payment or discount that lowers that price.

- Acquisition fee: a one-time fee the bank charges to start the lease, usually $600 to $1,000.

- Disposition fee: a fee you might pay at the end if you return the car and walk away, often around $350.

- Drive-off fees: just a catch-all term for everything you pay on day one.

- Loyalty or conquest cash: discounts for either sticking with a brand you already drive, or switching over from a competitor. These can knock $1,500 or more off a deal, but you only get them if you actually qualify.

That last one is important. A lot of advertised payments quietly assume you’re a returning customer or have great credit. Always check who the deal is actually for before you fall in love with the price.

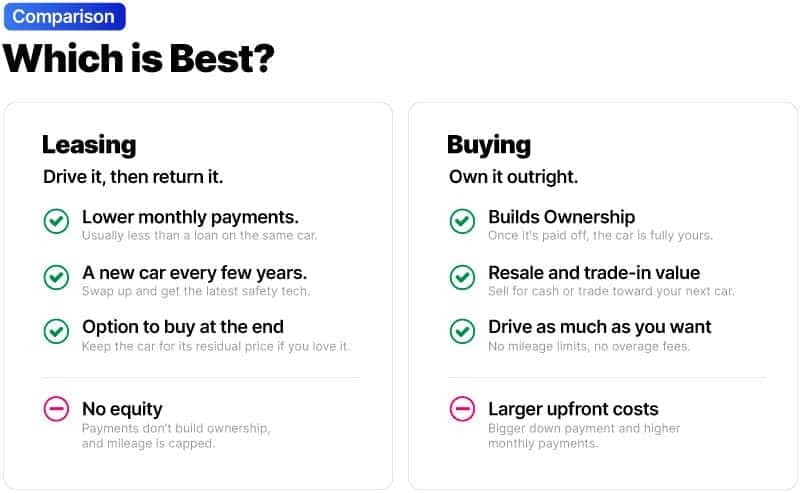

So… Lease or Buy?

Torn between leasing and buying and not sure what to choose? A quick way to figure out where you land: lease if you want a lower monthly payment, a new car every few years, and you don’t rack up crazy miles, just know you won’t own it at the end. Buy if you want the car to actually be yours someday, plan to keep it a long time, and drive a lot, just expect bigger payments and more cash upfront. Want the newest car for less each month? Lean lease. Want to own something down the road? Lean buy. Either way, we’ll walk you through the real numbers, no pressure.

A Couple Honest Caveats

Lease offers change depending on where you live, so the exact numbers you see online might be a little different locally. Your credit also affects what you qualify for. And taxes and fees usually stack on top of the advertised payment. None of this is shady, it’s just how leasing works everywhere, so it’s good to know going in.

A great lease isn’t the one with the lowest monthly payment. It’s the one with the lowest real cost (the effective monthly cost), on a car that holds its value, with enough miles for how you actually drive, and a deal you actually qualify for.

So do this: figure out the effective monthly cost, keep your upfront cash low, and make sure the mileage fits your life. That’s it. And because Walser doesn’t negotiate, the number you’re quoted is the real number, so the only thing left for you to do is make sure it fits you.

If you’re new to all this and still have questions, that’s completely normal. Come ask. Nobody expects you to walk in already fluent in lease-speak, and there’s no pressure either way.

For a free copy of your credit report, visit www.AnnualCreditReport.com or call 1-877-322-8228.

Avoid the Sticker Shock. Buy Now Before Tariffs Take Effect! March 31, 2025 Major auto tariffs are set to take effect on April 3, and industry experts predict that new vehicle prices could rise by thousands. If you’ve been thinking about buying a…

Avoid the Sticker Shock. Buy Now Before Tariffs Take Effect! March 31, 2025 Major auto tariffs are set to take effect on April 3, and industry experts predict that new vehicle prices could rise by thousands. If you’ve been thinking about buying a…New Vehicles, News, Used Vehicles

Selling Your Car Before Moving Out of State? Here’s How to Do It Without the Stress. February 25, 2025 The "Oh No, My Car" Moment Picture this: You’re knee-deep in moving boxes, drowning in packing tape, and questioning every decision that led to owning so many coffee mugs. Then,…

Selling Your Car Before Moving Out of State? Here’s How to Do It Without the Stress. February 25, 2025 The "Oh No, My Car" Moment Picture this: You’re knee-deep in moving boxes, drowning in packing tape, and questioning every decision that led to owning so many coffee mugs. Then,…WalserBuysCars

What’s in My Budget: Finding a Vehicle Priced Under 10K June 25, 2024 Are you in the market for a new ride but working with a tight budget? No worries! Finding a reliable and affordable vehicle priced under $10K is possible, and we’re…

What’s in My Budget: Finding a Vehicle Priced Under 10K June 25, 2024 Are you in the market for a new ride but working with a tight budget? No worries! Finding a reliable and affordable vehicle priced under $10K is possible, and we’re…Under 10k, Used Vehicles

What It Means to Live in a Severe Weather State: Minnesota Edition September 16, 2025 When you hear the phrase “severe weather state,” it might sound a little overly-dramatic. But, if you’ve lived in Minnesota long enough, you know it’s just a way of life.…

What It Means to Live in a Severe Weather State: Minnesota Edition September 16, 2025 When you hear the phrase “severe weather state,” it might sound a little overly-dramatic. But, if you’ve lived in Minnesota long enough, you know it’s just a way of life.…Maintenance, Minnesota, Safety